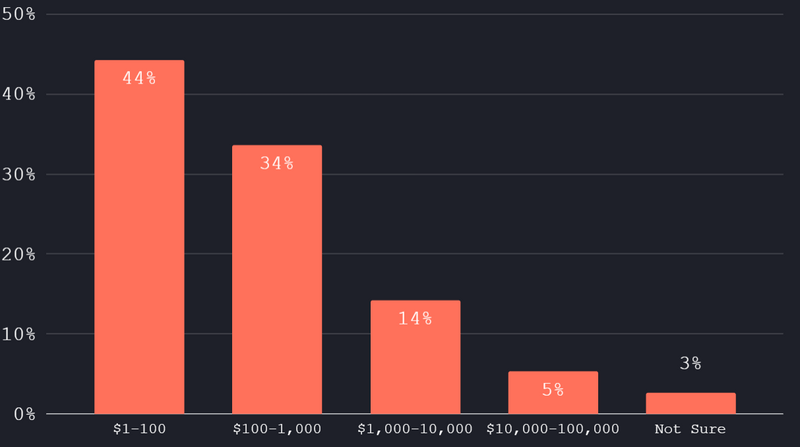

Which best describes your monthly Average Revenue Per Customer?

Expected:

There’s a wide spread of average price points for SaaS companies. Between the target market, value delivered, and category norms, there’s no such thing as a perfect price.

Unexpected:

This paints a pretty good picture between businesses that are primarily product-led growth with a lower average price point vs businesses that are primarily sales-led growth with a higher average price point. However, I would have originally expected the split to be pretty 50/50, or at least 60/40. Instead it’s about 75/25 in favor of a lower price point.

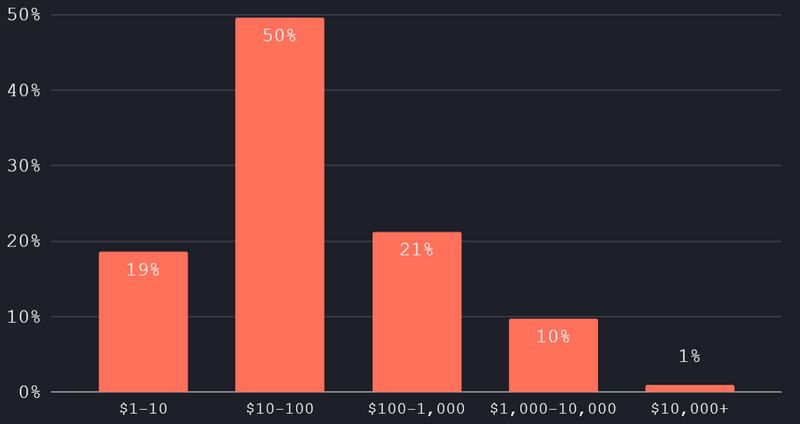

Which best describes the pricing plan for your lowest-cost pricing tier on a monthly basis?

Expected:

The lowest price point mirrors the ARPC from the last question pretty closely, which is a good indicator that the majority of customers are on lower priced plans, if not the very bottom plan.

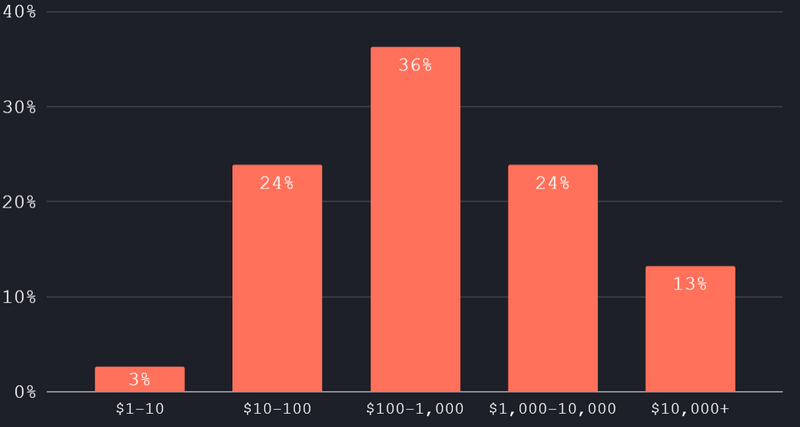

Which best describes the pricing plan for your highest-cost pricing tier on a monthly basis?

Unexpected:

Almost every company that has a starting price point between $1-10/mo also offers larger price points. It’s rare to only offer arange of plans between $1-10/mo.

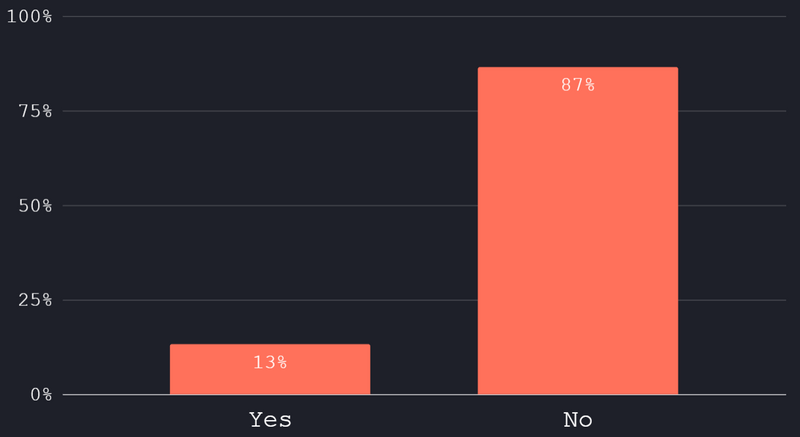

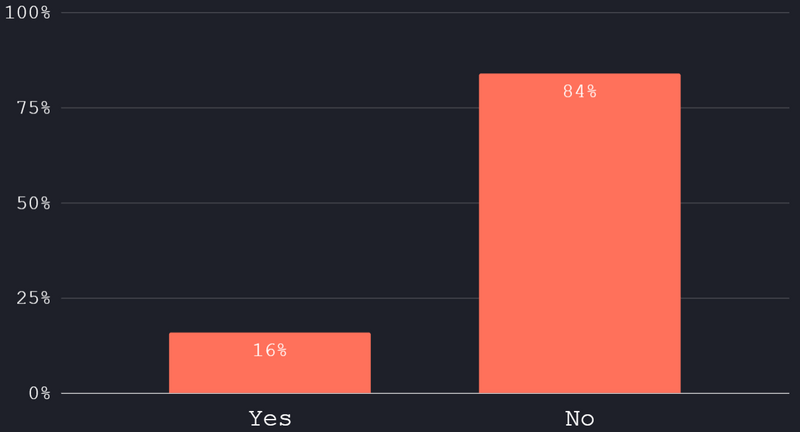

Do you offer a free trial for your product?

Unexpected:

I originally expected a lot more companies to respond with “Yes” since it feels pretty ubiquitous across the board when looking at pricing pages and calls to action on homepages. And given the dynamics of the ARPC listed previously, I would expect to see more product-led growth models.

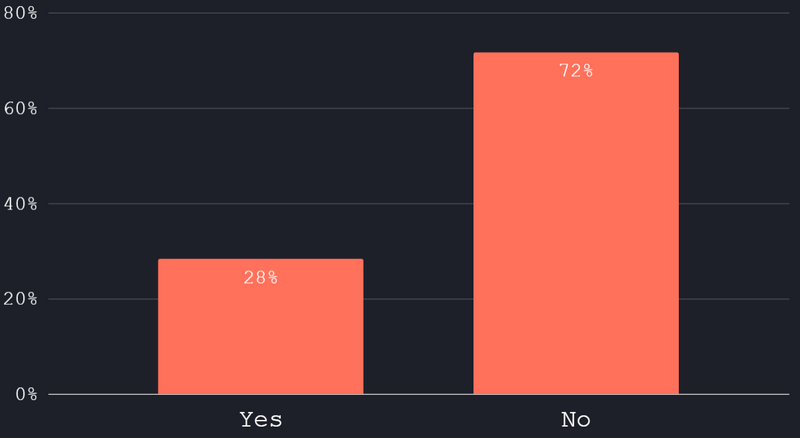

Do you offer a forever-free plan?

Unexpected:

After not seeing many mentions of free trials, I would have expected to see more mentions of free plans.

It’s possible that freemium models are the dominant model, which just isn’t being represented in the survey here. Many freemium models today are more akin to a usage-based trial, which may not be accurately described as a free trial or forever-free plan.

Do you charge a setup fee?

Expected:

Setup fees are pretty rare, with the exception of larger ARPC deals that require a lot of time from a customer success manager or solutions engineer.

Unexpected:

13.3% is actually a pretty significant number. Given the breakdown of ARPC we saw earlier, this would suggest a meaningful portion of companies with high ARPC do charge a setup fee.